We define the delivery quantity that more than 3 square meters as medium size and small volume orders. define the 3-50 square meters orders as small volume orders and the 50-200 square meters orders as medium size orders.

In recent years, there has been increase in demand for low volume so as to obtain first preference for small volume Circuit Board manufacturing; hence we created unique capabilities for catering these services.

We are generally capable of manufacturing from one layer PCB to multilayer as per customer specific board types like FR4, High TG FR-4, Rogers. we are even capable of manufacturing Maximum Panel/Board size 19.7" X 31.5", PCB Thickness 8 mil to 240 mil, Minimum Track Width & spacing 3 mil, Controlled impedance, smallest drill Hole 6 mil, etc.

Medium Size And Small Volume PCB Medium Size PCB,Small Volume PCB,Economical Medium Size PCB,Medium Size PCB Design Orilind Limited Company , https://www.orilind.com

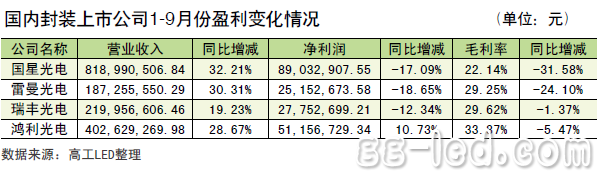

According to the data of the three domestic LED packaging listed companies (National Star Optoelectronics, Lehman Optoelectronics, Ruifeng Optoelectronics, Hongli Optoelectronics), the gross profit margin and net interest rate both showed different degrees of decline.

The below-period performance growth and drastic price-cutting storms have made this year's domestic LED packaging industry quite a bit chilly.

The industry turning point is approaching, the market pattern dominated by the middle and low end or facing a new round of industry reshuffle, and enterprises with core competitiveness in brand and technology still have a large development space.

The adjustment period is also the moment when the change appears. In addition to the reshuffle inside the domestic enterprises, the hands outside the wall are also coming in. Since 2010, multinational companies including Samsung, LG, CREE, and OSRAM have deployed LED packaging bases in China, on the one hand to better meet the needs of the Chinese market, and on the other hand to further control the high-end market.

In the high-end market, domestic packaging manufacturers have not emerged. In the eyes of the industry, this is quite dangerous. The high-end market is the main source of profit, and it is also the point of creation of corporate brands. Losing high-end means losing control of the value chain.

Growth is lower than market expectations

The huge contradiction between the weak growth of downstream application market demand and the rapid growth of upstream capacity supply is the general consensus of the LED industry.

"Although the penetration rate of global LED TVs has increased from 20% to 40% last year, the LED technology is increasing and the application is mature (the number of LED devices used in wattage strips is correspondingly reduced), which actually causes the absolute LED this year. The number has not increased too much.†Gong Weibin, chairman of Ruifeng Optoelectronics, said that the lighting and backlight market, which is the focus of LED applications, did not have the expected growth rate.

According to the data, domestic LED packaging listed companies have shown a slowdown in earnings from January to September this year. Among them, the net profit of the four companies only Hongli Optoelectronics showed a rising trend, and the other three have different degrees of decline; while the gross profit margins of key indicators reflecting the profitability of the company's operating profit, the four companies showed a downward trend without exception. Its China Star Optoelectronics and Lehman Optoelectronics have fallen by more than 20 percentage points.

The decline in the profitability of listed companies also represents the overall development status of domestic packaging companies. According to the statistics of the High-tech LED Industry Research Institute (GLII), compared with the profit of more than 90% of LED packaging companies in China in 2010, the proportion of loss-making enterprises will increase significantly this year. At the same time, GLII estimates that China's LED packaging output value this year is 32 billion yuan, an increase of only 18% compared with last year, far below the market growth rate of more than 30%.

"The trend of price reduction of packaged products is impossible to alleviate. Now the demand for the market is increasing. The biggest driving force is the price reduction of products." Zhang Canguang, deputy general manager of Guangzhou Hongcai Electronics Co., Ltd., a subsidiary of Taiwan's Shunhong Group, pointed out. From the development level of technology, there is not much room for the cost of accessories in the lighting part, and the real space for the large drop is the light source. Therefore, the price of the light source will decrease, which will lead to the decline of the entire lamp cost.

In the past few years, the cost of LED fluorescent tube light sources on the market accounted for 60% to 70% of the total cost of lamps. By this year, it has been estimated to have dropped to 40%-50%. However, Zhang Canguang also said that the price of the light source will not drop all the time, there will always be a bottoming position. "Unless the packaging technology has a new qualitative change, the price will naturally have a subversive decline. The new quality change is that the light efficiency reaches a certain level or above, and no more heat treatment is needed." Zhang Canguang believes that "some Level" means light efficiency over 200lm/W. ![]()

The growth is lower than expected LED packaging industry "mountain rain"

[High-tech LED News] (text / reporter Hu Yanling) Things must be reversed, when industrial investment is getting more and more fire, the signs of homogenization competition are beginning to appear. In particular, some weaker competitors are rushing in and pushing low-priced products, and the entire industry will inevitably suffer the impact of falling gross profit.